Every investment is completely different from the last. Kai asked the following question in chat: -

”would you still buy ZIM today if you did not already own it? Just wondering how viable it is without the big dividend?”

It’s rare to say you invest in a business irrespective of whether the market conditions makes sense, however, Zim is that company for me. To answer the question briefly before breaking it down, no, I wouldn’t be adding to the position today but I still expect more upside from here.

Table of contents:

Net-net investing, commonly knows a “cigar butts”

Market environment and risks associated with Zim

Wrapping up with my expectations moving forward

1. Net-net investing

The term “cigar butt” was commonly referred to Benjamin Graham’s value investing style of “net-net” investing. The idea behind it, was to find a company with strong current assets where inventories and receivables were marked down as bad credit or liquidation stock yet the company would still have a sufficient amount of liquid cash available after paying down total liabilities.

How does that related to Zim?

Fiscal stimulus in 2020 led to an incredible ramp up in spending on good thus driving freight rates up 5 to 6 times. The HUGE cash windfall from many of these operators was used to de-risk their business and effectively cutting their debt to zero and allowing for the excess cash to generate interest incomes on the excess cash balances. Shipping went through a major turnaround.

Zim is not a typical net-net, however, it offered significant value. Non-current liabilities are roughly 54% of the companies “Vessels” & “Containers and handling equipment”. Zim could afford to liquidate their fixed assets at a 46% discount and still cover their non-current liabilities.

So whats its worth?

If we take cash & equivalents, short term investments, receivables & their liquid long-term assets and divide it by their current liabilities, the company is worth $23.23 conservatively.

2. Market environment and

The above valuation is purely based on the liquid value of the company and its entirely indifferent to market conditions. This matters, in a highly cyclical market costs can easily outweigh income and a cyclical business can haemorrhage cash in anticipation of a market cycle turn.

So although we scratched the surface above looking at the opportunity as a “cigar butt” we need to have a little more detail on where the shipping cycle is and how that impacts Zim directly.

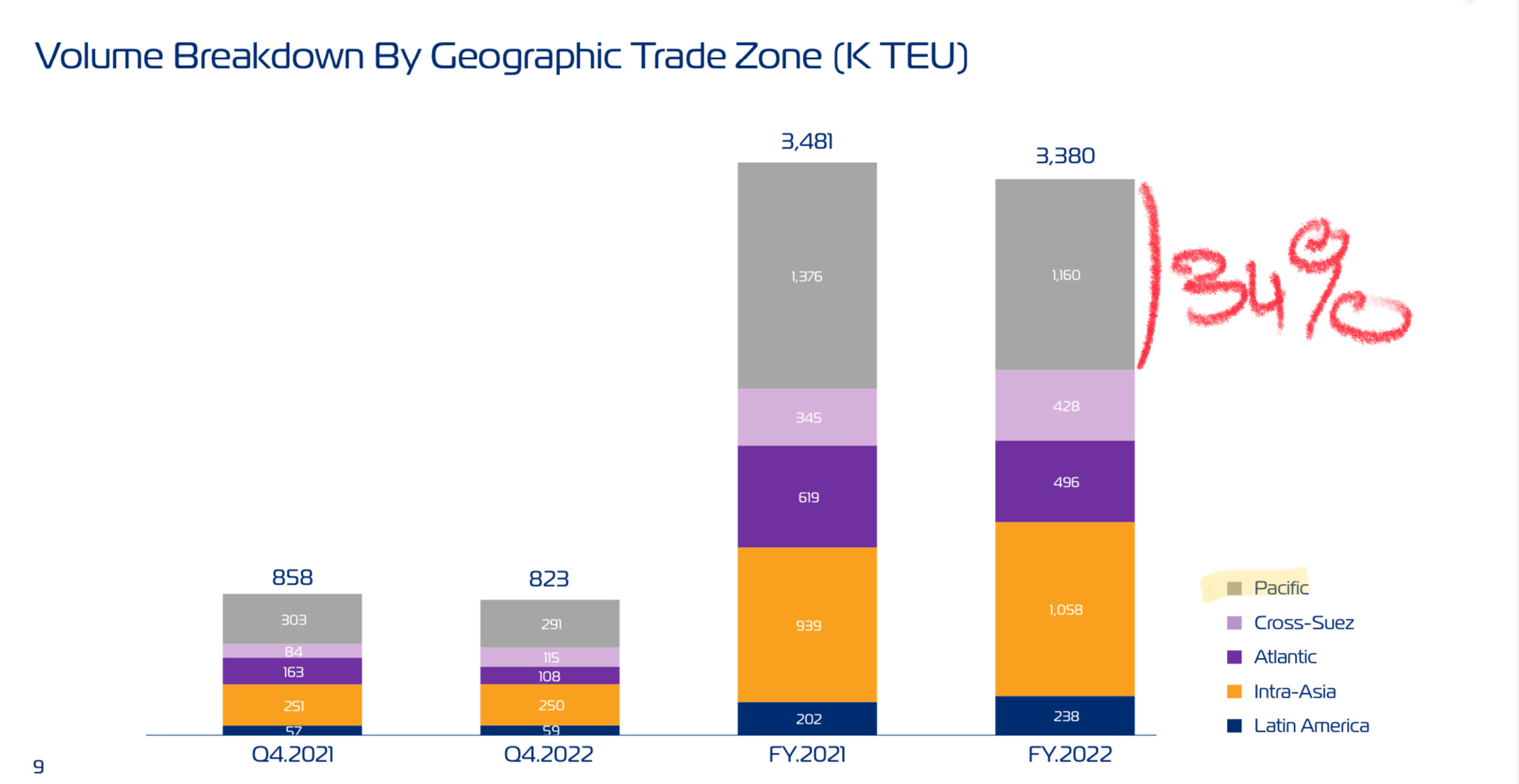

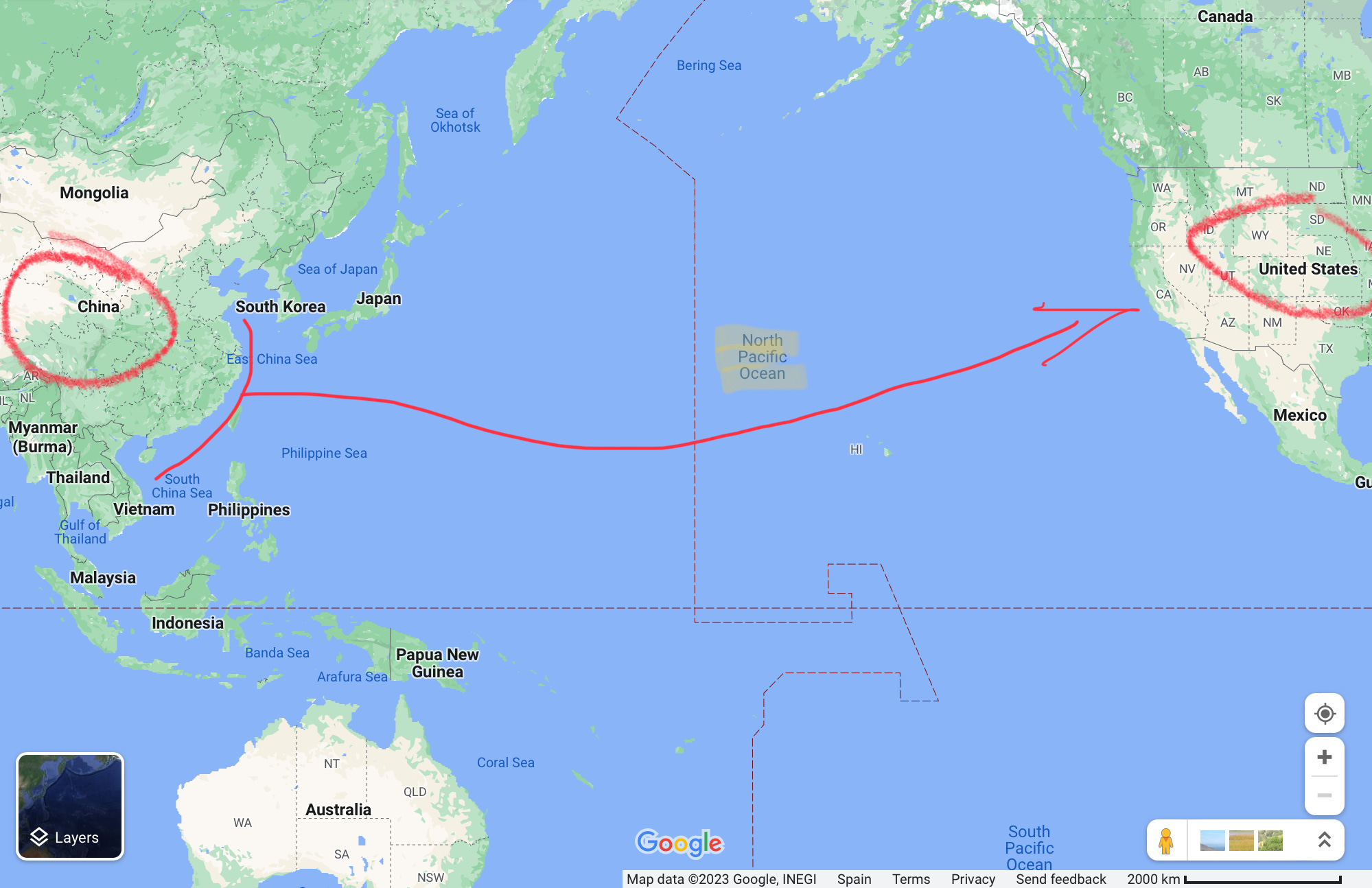

34% of Zim’s volume comes through the Pacific Ocean.

Looking at a map, it connects China to the United States, and with China disclosing back in November last year their intent to reopen it wouldn’t take much to support Zim. Remember, we looked at it from a liquidation perspective, if earnings were flat we still believe the company to be worth $23.23 conservatively.

Since November, the Dry Bulk Index which measures the cost of shipping goods worldwide is up roughly 16% after stabilising in early 2023 and rebounding. In hindsight, whether this is related to China or not (I suspect it is), Zim is in a slightly better predicament today vs last November with gas prices down and freight rates up.

We can say at least up to the present day, the market has stabilised for shipping companies.

3. Expectations from here

I averaged into Zim on two ocassions, on November 2nd and again on December 12th for an average entry of $22.46.

Since acquiring the share, Zim has paid out two dividends, $2.95 on November 28th and $6.40 on April 4th to total $9.35. When a company makes a decision to payout a dividend its a distribution off the company’s balance sheet from current assets and out the door into my bank account. Part of the remuneration has come in the form of dividends and today we expect the equity to be worth $23.23 offering up a $0.77 capital gain.

The total return from the investment, if and when price hits our target the total return will equal $10.12 per share or 45%.

The company could pull together, earnings could grow at a faster pace and we could certainly see much higher prices in the weeks and months ahead given the trend on the dry bulk index, however, that’s not why I entered the position. Zim was a company trading far too cheap relative to its liquid cash and the expectation was to see a mean reversion. For that reason, I don’t plan to build out the position further and I wouldn’t be considering entering at this juncture.

Its not a directional play, on the market, but a net-net where the company was far too cheap.

As of today, my plan remains to exit at least half if not all of the position on a trip back up to $23.23.

Share this post